This study first appeared in Montel’s Geopolitical Report – March 2026.

Geopolitical Escalation and the Strategic Importance of the Strait

In the early hours of Saturday, 28 February, coordinated U.S. and Israeli strikes targeted sites in Tehran, marking a significant escalation in hostilities. The strikes followed several weeks of rising tensions between the United States and Iran, including increased US military positioning in the region and heightened diplomatic strain surrounding Iran’s nuclear programme. Iran has since responded with attacks on US and allied positions in the region. The situation remains fluid, with the potential for a prolonged period of regional tension and disruption.

A protracted conflict would increase the risk of disruptions to shipping through the Strait of Hormuz, a critical chokepoint for global LNG trade. The waterway handles the transit of virtually all LNG exports from Qatar, one of the world’s largest LNG exporters, as well as volumes from the UAE. According to RBAC’s latest estimates, combined LNG exports from these two countries exceed 80 mtpa in 2025, representing nearly 19% of global LNG trade.

Most of these volumes are directed to Asia under long-term contracts. China and India are the primary destinations, with LNG cargoes transiting via the Strait of Hormuz accounting for around 25% and 50% of their total LNG imports respectively. Japan and South Korea also import significant volumes of Qatari and UAE LNG. While total import volumes are smaller for Pakistan and Bangladesh, these markets are more heavily dependent on Qatari supply, which accounts for roughly 90% and 70% of their LNG imports respectively.

Europe is comparatively less reliant on LNG transiting via the Strait of Hormuz. EU imports from Qatar totaled approximately 10mtpa in 2025, with Italy accounting for the largest share.

Looking ahead, Qatar’s planned expansion is expected to be a major driver of global LNG supply growth over the next two years, with approximately 32mtpa of additional capacity scheduled to come online from late 2026 onwards.

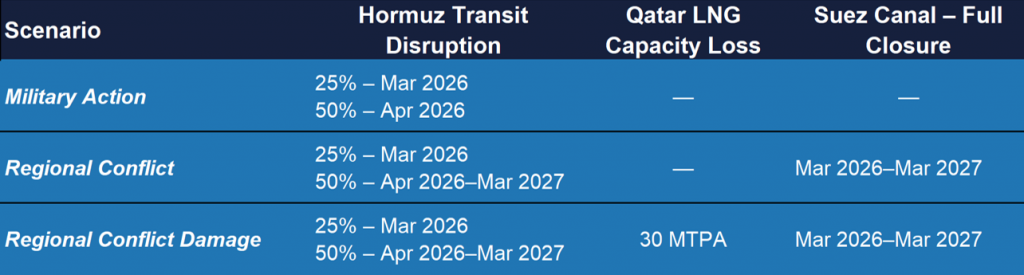

Given the scale of these volumes, any sustained disruption to trade through the Strait of Hormuz would have a material impact on global LNG balances, prices and trade flows. To assess the potential impact, this analysis uses RBAC’s G2M2 global gas market model to simulate three disruption scenarios, summarised in Table 1.

The first scenario, Military Action, assumes a short conflict lasting two months. The second scenario, Regional Conflict, models a more prolonged escalation in which LNG trade via the Strait of Hormuz is curtailed by 50% for 12 months.

The third and most severe case, Regional Conflict Damage, assumes damage to Qatari LNG liquefaction infrastructure following an attack by the Iranian military or one of its proxies, which has already materialised. Although the damage remains uncertain, the modelling assumed a 30 mtpa reduction in output for 12 months after the conflict. Production is then assumed to ramp back to nameplate capacity between 2028 and 2029.

The Regional Conflict and Regional Conflict Damage scenarios also assume that transits via the Suez Canal are stopped as a result of a resumption of Houthi attacks on shipping. This is expected to continue for as long as the conflict lasts. The results for these three scenarios have been compared to a Base Case in which no disruption to trade via the Strait of Hormuz occurs.

Market Context Before the Disruption

Before analysing the impact of these disruption scenarios, it is important to outline the forces that were expected to shape global gas markets over the next five years prior to the recent escalation. The 2025–2026 winter has left European gas storage at its lowest level for this time of year since the start of the Ukraine–Russia conflict, approximately 35–40% below the three-year seasonal average. As a result, Europe is likely to require a material increase in LNG imports in 2026 to meet its stated storage-filling targets.

At the same time, Russia still accounts for approximately 15% of European LNG supply. With EU measures to phase out Russian LNG imports and related transshipment services by the end of 2027, alongside the sharp reduction in Russian pipeline gas flows since 2022, Europe’s available LNG supply pool is set to narrow further, increasing its reliance on alternative suppliers including Qatar and the UAE.

The anticipated increase in European LNG demand was expected to be accommodated by significant growth in global liquefaction capacity over the next 12 months, including a substantial expansion in Qatari export capacity as new North Field volumes begin to enter the market. Under pre-escalation assumptions, this supply growth was projected to exceed incremental demand from Europe in 2026, allowing prices to ease relative to the elevated levels seen over the past year and enabling stronger consumption growth in more price-sensitive Asian markets.

From 2027 onwards, further substantial additions to global LNG capacity, as projects currently under development come online, were projected to deepen the supply expansion, placing additional downward pressure on prices through to the end of the decade.

Price Impacts of Disruption

Introducing a disruption to trade through the Strait of Hormuz into this market environment results in a rapid tightening of the spot LNG market. Importers unable to receive volumes under long-term contracts would be forced to seek replacement cargoes on the spot market. The impact is especially pronounced in 2026, given the anticipated increase in European LNG demand associated with storage refill requirements. At the same time, the availability of flexible supply is limited, as U.S. LNG export facilities are currently operating at approximately 97–100% utilisation, with the majority of volumes contracted.

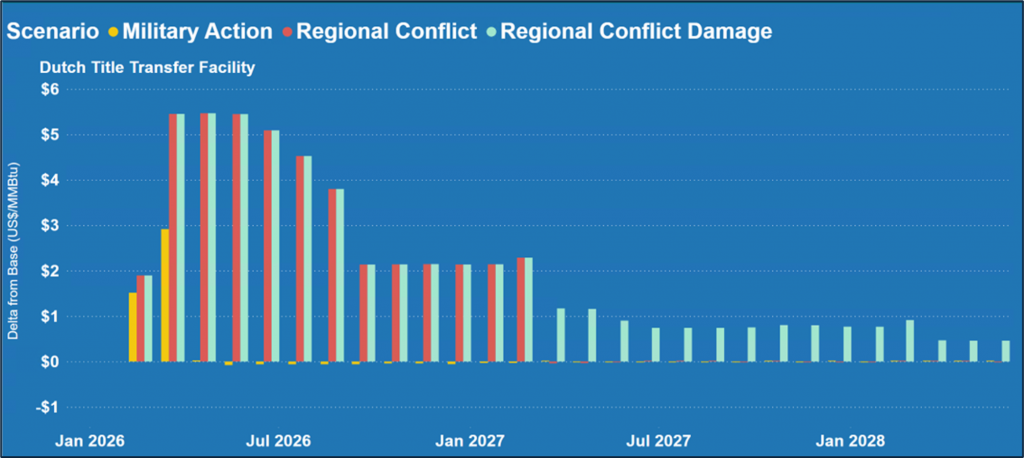

The impact on TTF prices under each scenario is shown in Figure 1, below. In the Military Action scenario, TTF prices rise by approximately USD2–3/MMBtu, reflecting the limited duration of the disruption. In the Regional Conflict scenario, the increase relative to the Base Case peaks at over USD 5.50/MMBtu in summer 2026 before moderating to around $2/MMBtu during the 2026–2027 winter.

Under the more severe Regional Conflict Damage scenario, price effects extend into 2027 and 2028, with average increases then of between USD 0.50/MMBtu and USD 1.00/MMBtu relative to the Base Case. While material, these impacts are not projected to match the extreme price spikes observed following the invasion of Ukraine, reflecting the comparatively smaller loss of global supply across the scenarios modelled here.

The anticipated expansion in global liquefaction capacity in the coming years also plays a moderating role, cushioning the market impact of a prolonged US–Iran conflict.

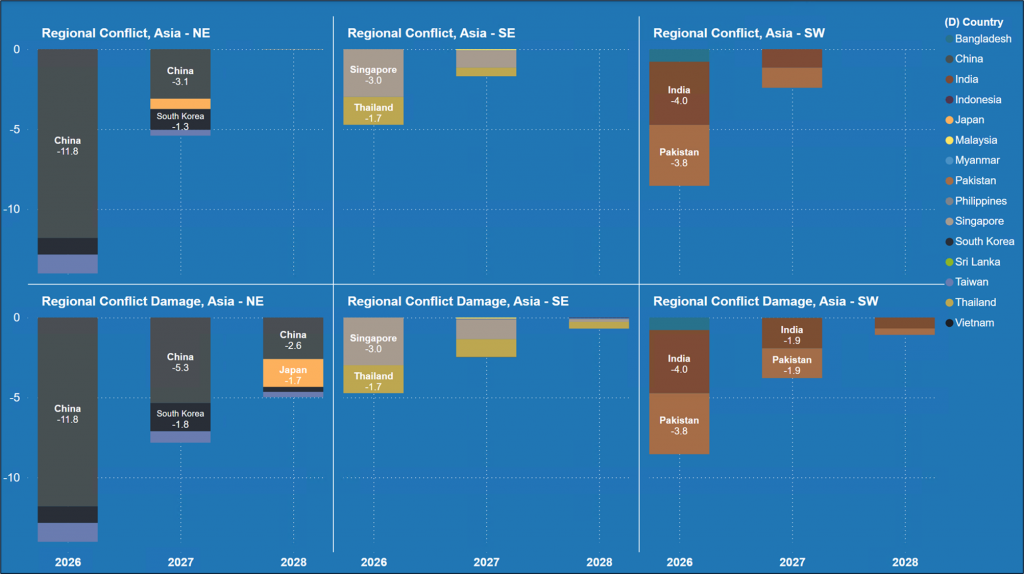

Demand Adjustment

The expected increase in spot prices as importers scramble to replace the lost supply is likely to lead to a reduction in demand from more price-sensitive segments of Asian gas consumption. This is shown in Figure 2, below. As a result, China and South Asia are expected to absorb the majority of the reduction in global supply across all scenarios. This would mirror the reaction to other sudden phases of market tightness in recent years. In the Regional Conflict and Regional Conflict Damage scenarios especially, Pakistan sees the most significant relative reduction in total LNG imports. This may result in supply curtailments and an energy emergency in the country in 2026. A similar crisis may also be triggered in Bangladesh given the significance of Qatari LNG imports in the country’s gas supply mix.

Higher spot prices are also projected to reduce European LNG imports, but by roughly one-quarter of the decline observed in Asia. Although European buyers source a smaller share of volumes through long-term contracts with Qatar, their exposure stems primarily from the region’s heavy reliance on spot LNG. As global spot prices rise, European import demand moderates.

This contrasts with the adjustment in Asia, where price-sensitive buyers absorb a larger share of the global supply reduction through lower consumption. In Europe, however, storage dynamics offset part of this price response. Storage levels are at their lowest point since the start of the Ukraine–Russia conflict, and the additional volumes required to refill inventories during the summer injection season (along with regulatory pressure to meet storage targets) are expected to maintain upward pressure on prices and constrain flexibility in import demand.

Market Resilience and Duration of Disruption

While uncertainty remains regarding how the conflict will evolve, the market reaction to date underscores the scale of the risk. Approximately 20% of global LNG trade transits the Strait of Hormuz, and Qatar represents a growing share of global supply. With limited spare liquefaction capacity outside the Persian Gulf and US LNG export facilities already operating near full utilisation, the system has little buffer against further disruption.

The central issue therefore, is duration. A short-lived interruption would likely result in temporary volatility. However, if shipping constraints and the halt of Qatari LNG production persist, low European inventories, tightening EU restrictions on Russian LNG and the already high utilisation of US LNG export facilities would significantly limit the market’s ability to adjust, sustaining materially higher prices for an extended period, particularly in Europe

###

Edward O’Toole is the Director of Global Gas Analysis at RBAC, Inc.

Giovanni Bettinelli is a Gas Analyst at RBAC, Inc.

RBAC, Inc. has been the leading provider of market fundamental analysis tools used by the energy industry and related government agencies for over two decades. The GPCM® Market Simulator for North American Gas and LNG™ is the most widely used natural gas market modelling system in North America. RBAC’s G2M2® Market Simulator for Global Gas and LNG™ has been instrumental in understanding evolving global gas and LNG dynamics and is vital in fully understanding the interrelationship between the North American and global gas markets.