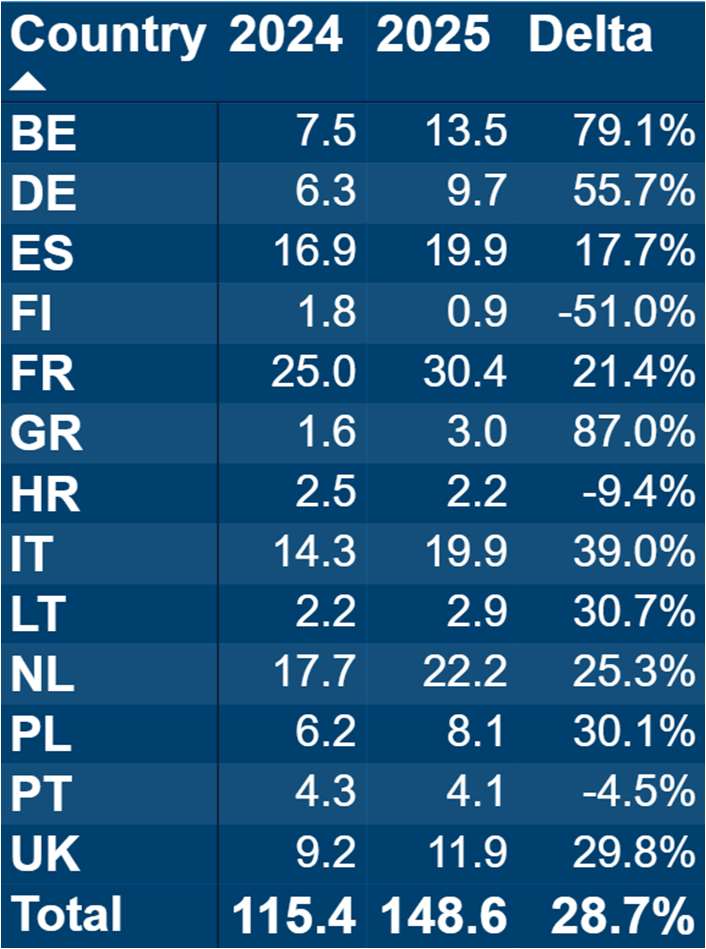

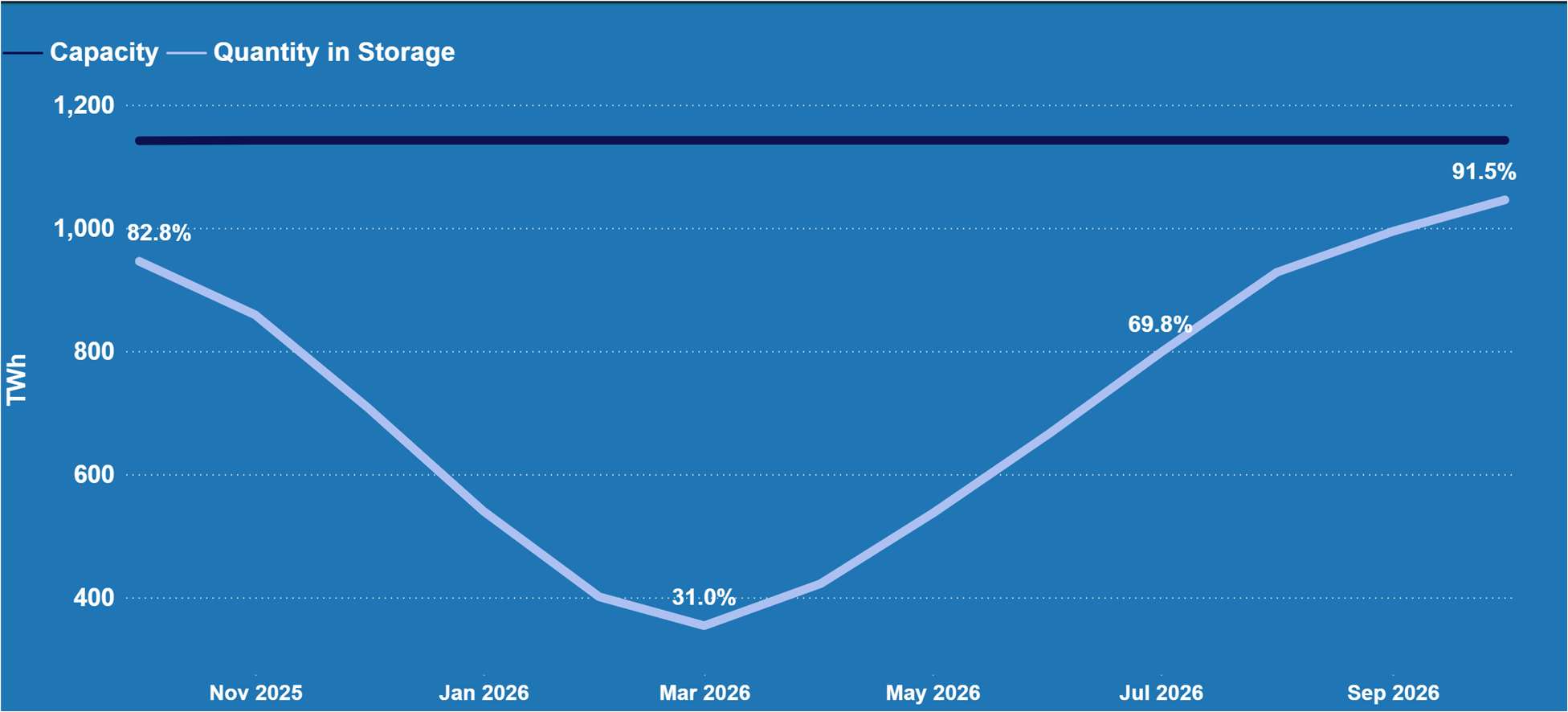

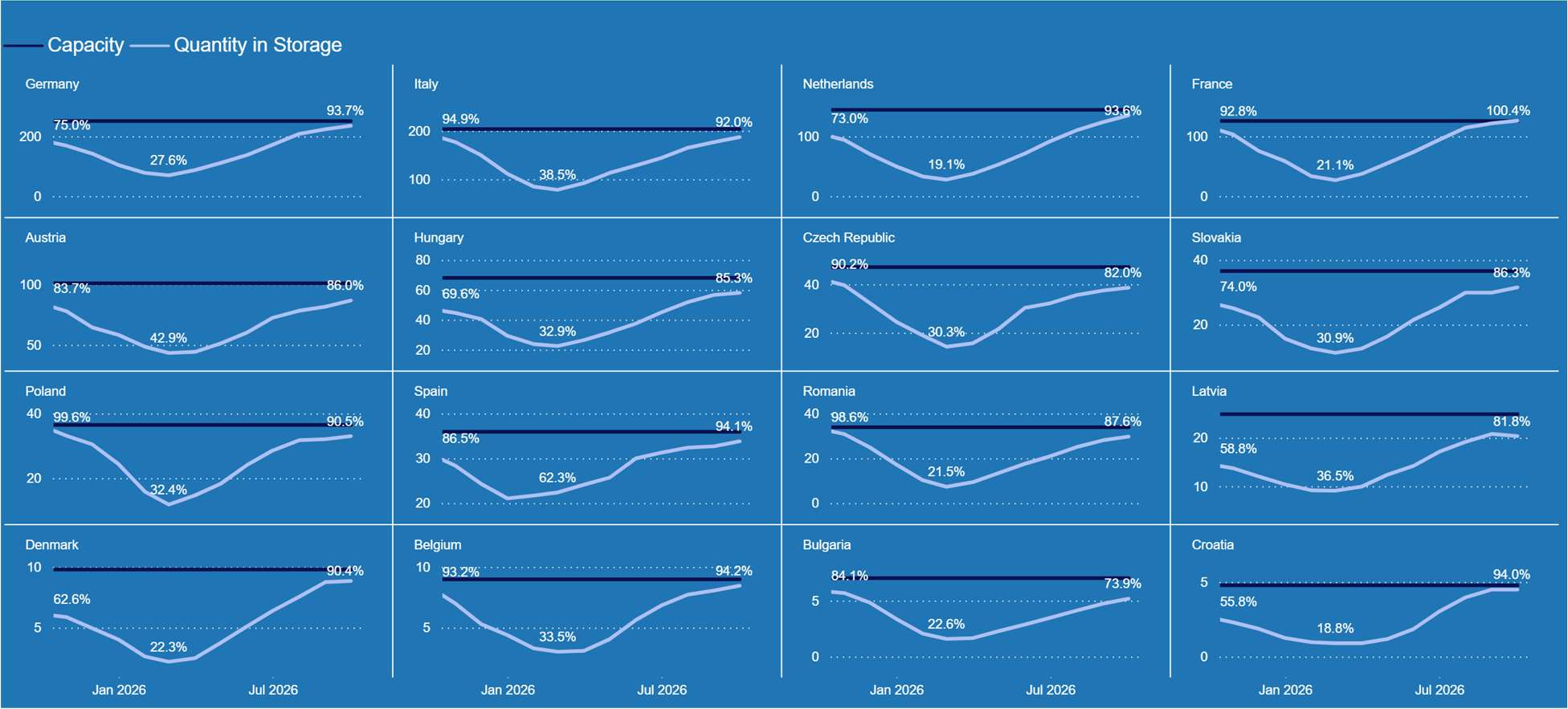

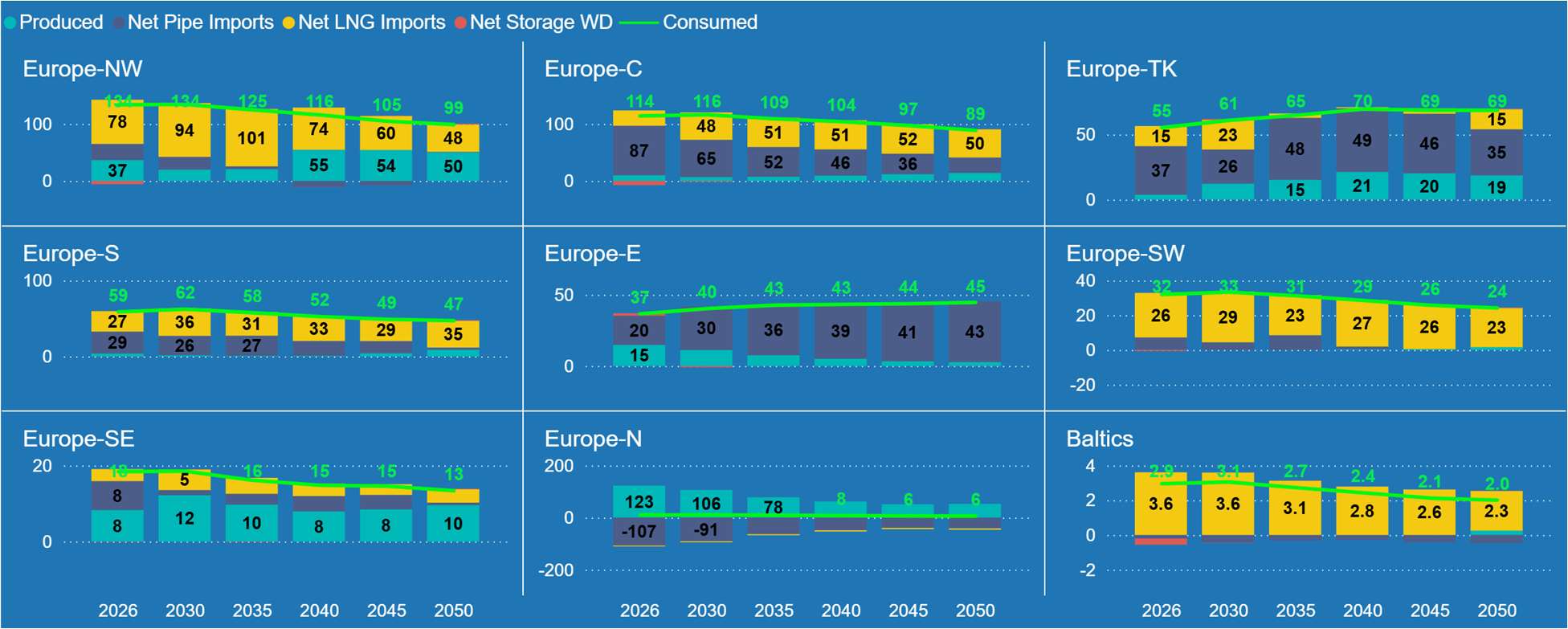

The 25Q4 release reflects key global trends and shifting market dynamics, such as in Europe, where we see lower-than-expected storage levels, tighter near-term supply balances following winter withdrawals, and the legally bound phase-out of Russian LNG by the end of 2026 and Russian pipeline gas by late 2027 under the REPowerEU framework.

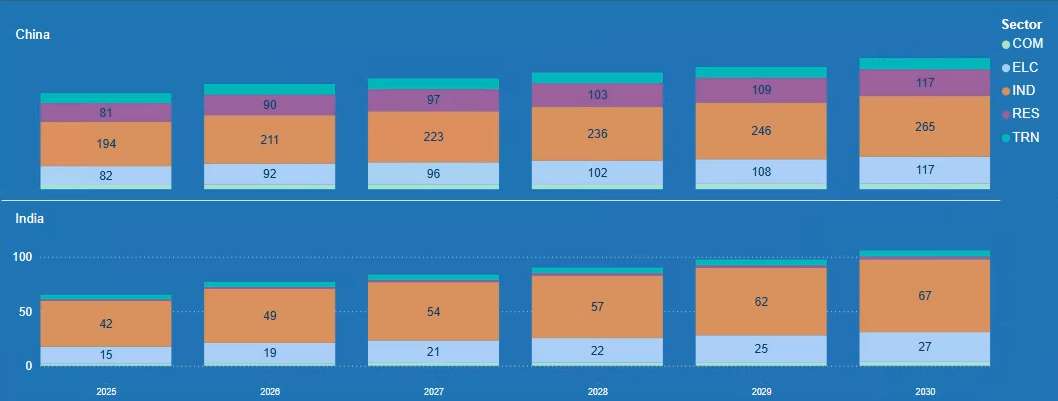

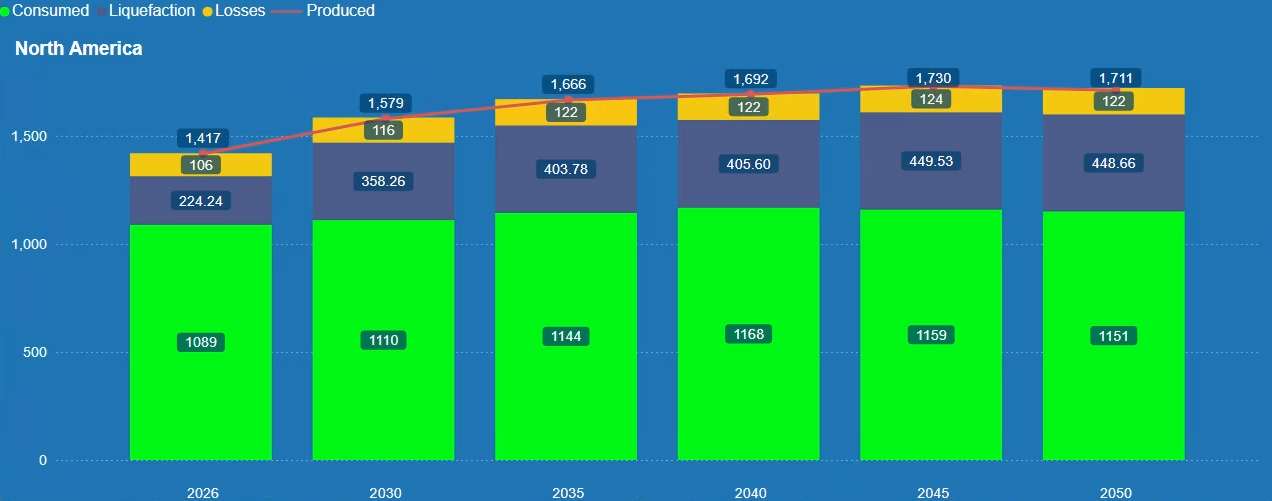

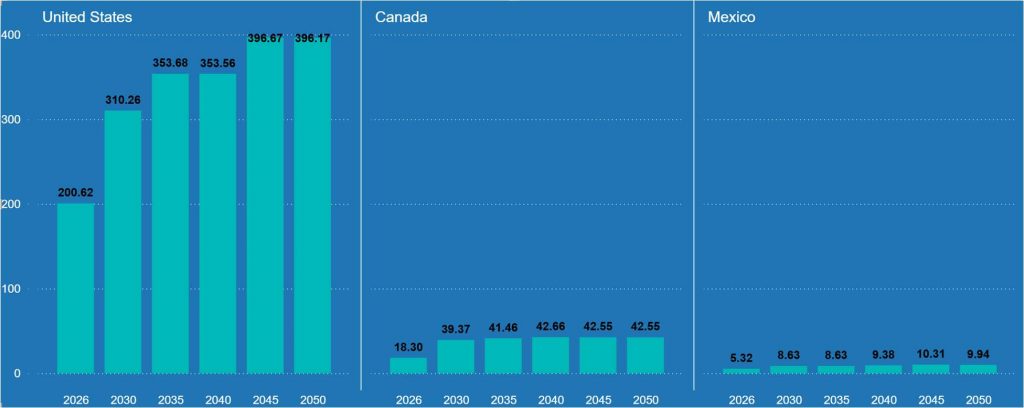

Asia remains a crucial driver of global natural gas demand, particularly with China, but India is also notable. While in North America, rising production is driven by LNG export growth, but also supports higher domestic gas demand, with the power sector leading incremental consumption.

In the medium term, while global liquefaction capacity continues to rise (in the U.S. and Qatar in particular), the outlook continues to point to a potential LNG supply surplus beginning around 2028, which is expected to place downward pressure on global gas prices. Beyond this period, sustained demand growth in Asia and the Middle East is expected to absorb excess supply, supporting a gradual price recovery into the mid-2030s.

It is with tools such as the G2M2® Market Simulator for Global Gas and LNG™ that natural gas and LNG analysts can see how changes in the market affect supply, demand, flows, and prices. For example, one can see how the implementation of the REPowerEU plan will result in new gas supply coming into Europe with Russian gas being fully phased out.

Would you like a demonstration of RBAC’s market simulation tools? Click here for a demo or to contact us for more information. Additionally, join our mailing list to receive articles and other communications from RBAC directly to your inbox.

RBAC, Inc. has been the leading provider of market fundamental analysis tools used by the energy industry and related government agencies for over two decades. The GPCM® Market Simulator for North American Gas and LNG™ is the most widely used natural gas market modeling system in North America. RBAC’s G2M2® Market Simulator for Global Gas and LNG™ has been instrumental in understanding evolving global gas and LNG dynamics and is vital in fully understanding the interrelationship between the North American and global gas markets.