Being able to export LNG would be of great benefit to Egypt by bringing much needed foreign currency into the country to help pay-down skyrocketing foreign debt, increasing investor confidence and even perhaps enticing the large capital investments needed for long-term economic stability and energy security. And it does appear that the government has made serious efforts in this direction in 2023.

Egypt briefly saw a spike in its LNG exports as a result of the war in Ukraine. Its exports to Europe generated $8.4 billion USD. more than double the previous year’s revenues from LNG exports. However, in time, the high natural gas prices came down and Europe diversified its sources and found long-term suppliers, and this impacted Egypt greatly. “In April, Egypt’s trade deficit increased by almost 24 percent year-on-year, driven by a decline in the value of gas exports.” Egypt saw its LNG exports decline both in value and volume and finally vanish for a short period of time due to its own gas shortages. It could happen again if new sources of supply are not secured or current sources of supply not properly developed.

With uncertainty surrounding Egypt’s future gas supply, market analysts and policy makers must have the tools and knowledge necessary to explore all options available. This could involve ramping up domestic production for consumption and LNG exports or increasing imports through new pipelines and/or LNG import terminals.

Using Market Simulation to Assess Egypt’s Natural Gas Future

RBAC’s G2M2® Market Simulator for Global Gas and LNG™ can be used to assess the viability and effects that any project or change in policy would have on supply, demand, prices, and gas flows.

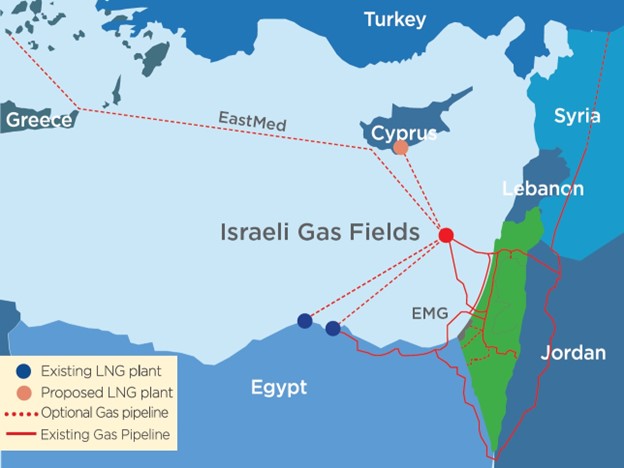

RBAC recently conducted such an analysis to investigate what might happen to the Egyptian gas market if pipeline imports from Israel were cut-off for the rest of this decade. As discussed earlier, the Arish-Ashkelon pipeline is the only source of gas imports for Egypt.

In the scenario where Egypt is not able to obtain a new charter for an FSRU to provide LNG imports, it would be dependent totally on domestic production for its natural gas supply. How would this affect the availability of gas for local consumption and for LNG exports?

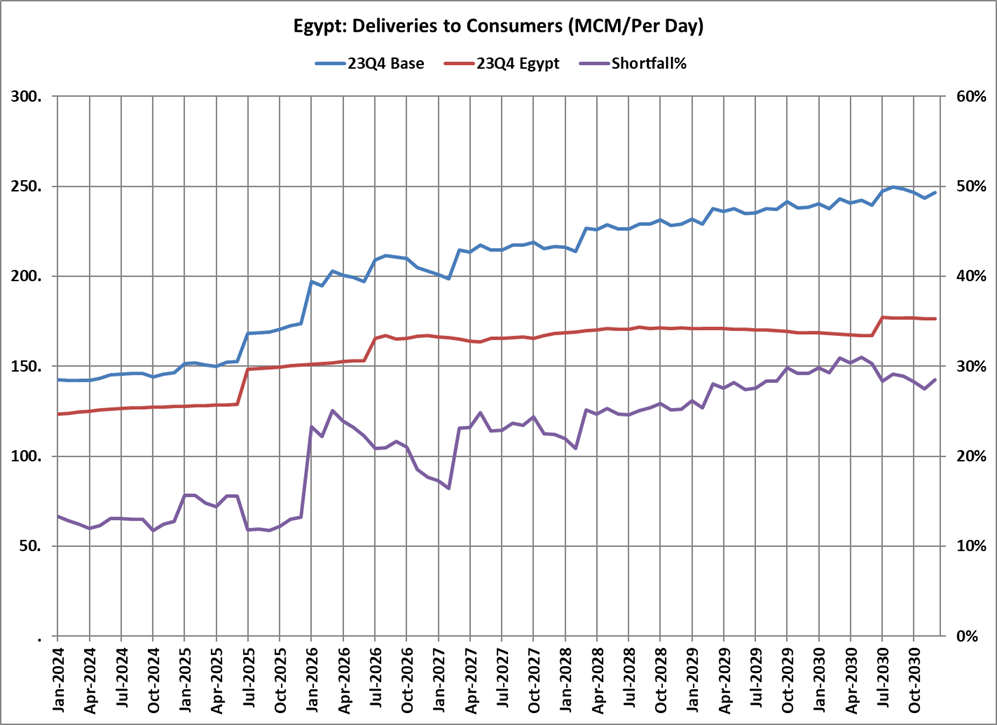

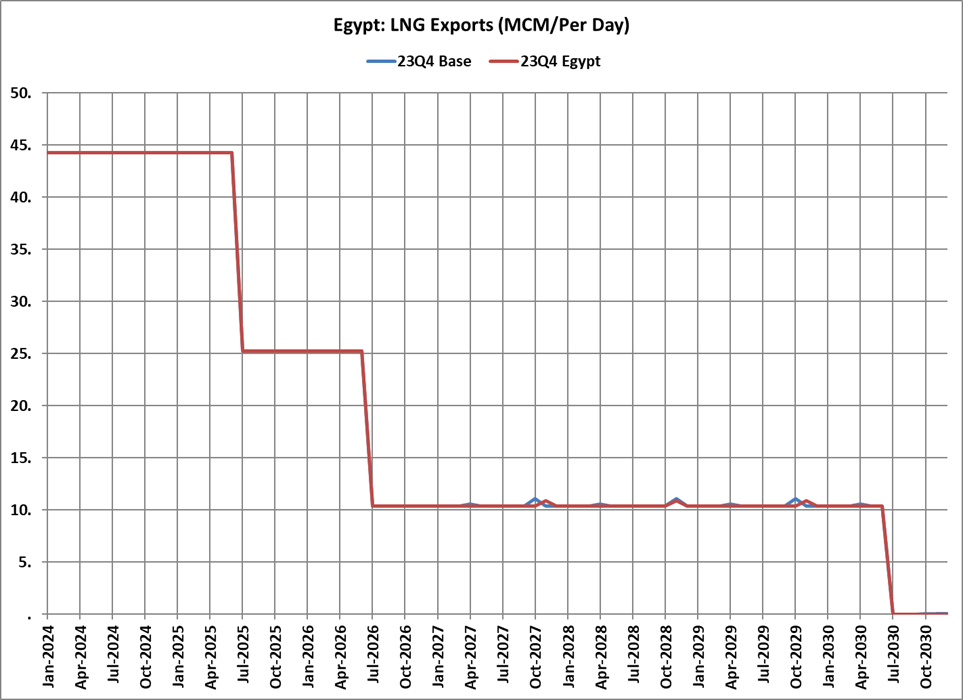

Using G2M2, analysts at RBAC prepared two scenarios: 24Q3 Base (business as usual) and 24Q3 Egypt (cut-off Israeli pipeline imports 2024-2030). The charts below show the results.