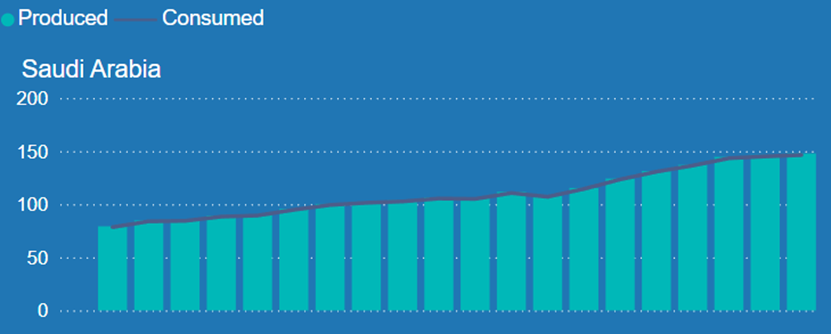

Saudi Arabia is primarily known for its vast oil reserves which has contributed to the rapid economic development in the country. Saudi Aramco (also Aramco) has grown to be one not only the largest energy company in the world, but one of the largest across all industries.

The $100 Billion Investment

After great success in oil, Saudi Arabia is looking to do the same in another energy segment. It is betting on natural gas to be its energy of the future, and to create this future, the country is investing $100 billion to become the third-largest shale gas producer, leveraging the 229 Tcf of confirmed gas reserves in the Jafurah field. This investment will overhaul the natural gas industry by 2030. Aramco is allocating $25 billion for plant construction and related work, with production starting in 2025. Aramco’s CEO Amin Nasser recently explained that the next phase involves expanding the gas network, adding 4,000 kilometers of pipelines, boosting capacity by 3.2 billion standard cubic feet per day, and connecting several additional cities. [1]

These investments come at a crucial time with demand steadily rising since 2011 and is expected to continue to do so in the coming decades. Alongside the development of the Jafurah gas field, Saudi Arabia is also looking to expand the processing capacity of the Fadhili gas plant. This expansion, targeted for completion by 2027, would increase capacity to 2.5 to 3.8 Bcf/d. [2]

LNG Becoming Additional Source of Supply

So far domestic production has been able to keep up with domestic consumption, but if additional gas supply were to be added into the mix, exports would also become an option for Saudi Arabia. This additional supply would come from a mix of increased domestic production and LNG imports, which are being looked at as an option. In fact, there is already an agreement to purchase LNG from the Port Arthur LNG project in Texas. [3] This would be for 5 MTPA over 20 years once the proposed second phase of the project is completed. However, the second phase of this project is still in the very early stages and still has regulatory, permitting, and financial hurdles to clear. The first phase is still under construction and trains one and two are expected to begin commercial operations in 2027 and 2028.

Prior to this agreement, there was also one made with NextDecade in which 1.2 MTPA within the same timeframe would be imported from the Rio Grande LNG facility, also in Texas. [4] However, a U.S. Court of Appeals recently revoked the permit issued by the Federal Energy Regulatory Commission for this project which leaves its future status up in the air. The construction for phase 1 of Rio Grande LNG is currently proceeding as planned and is expected to be completed by early 2029. This court ruling is expected to impact the FID status of the fourth train which was supposed to be given the greenlight late 2024.

Acquiring LNG Export Assets

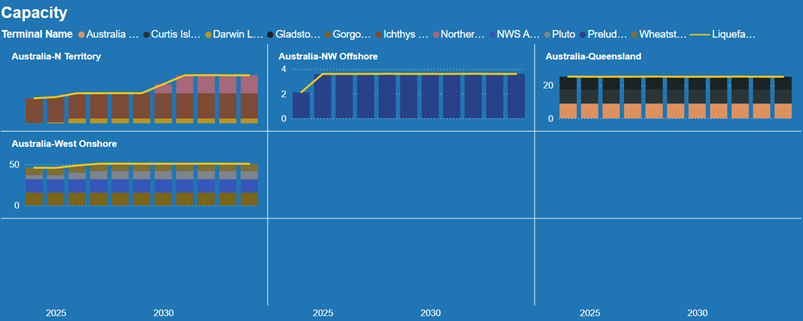

Saudi Arabia’s primary LNG partners are currently the United States and Australia. Following the deals struck with U.S. suppliers, it has also been making moves in Australia. Last year, Aramco acquired a minority stake in MidOcean Energy for $500 million.[5] MidOcean Energy is a U.S. based company that has several investments in Australian LNG projects and has overall goals to create a “diversified global LNG business.” Some of these projects include Gorgon LNG, Pluto LNG, and Queensland Curtis LNG projects.[6] Prior to the coronavirus pandemic, Aramco had even hired LNG traders in Singapore and was in negotiations with LNG producers; but these broke down due to the ensuing economic panic caused by the worldwide lockdowns.

In addition to assets in Australia, it also holds a 20% stake in Peru LNG as of April 2024.[7] All of these investments make it clear that Saudi Arabia fully believes in the future of natural gas and LNG and is going to great lengths to ensure that it is a part of this future. In the words of Aramco CEO, Amin Nasser, “We should abandon the fantasy of phasing out oil and gas, and instead invest in them adequately, reflecting realistic demand assumptions.”[8]

Saudi Vision 2030

As a whole, the state-owned Aramco is targeting a, “60% Increase in Gas Production by 2030.” [9] Currently, the power generation mix within the country is 60% gas fired and 40% oil-fired. [10] However, there has been calls to end the emissions that are a byproduct of utilizing oil for power generation and replace it with increased usage of natural gas and renewables. “In line with the shift to shale gas, Saudi Arabia announced in January that it would halt plans to expand crude oil production capacity. It had planned to increase production by 1 million barrels per day to 13 million barrels per day by 2027.” [11] The cancellation of thee plans to increase oil production frees up $40 billion that would have been spent between 2024 and 2028.

Instead, there will now be an overhaul of the country’s current pipeline transportation system which Aramco signed a $1.3 billion contract with China’s Sinopec for construction. [12] Completion of this project is expected by May of 2027 and would bring gas to parts of Saudi Arabia that were using crude oil for power generation.

Movements in the Middle East

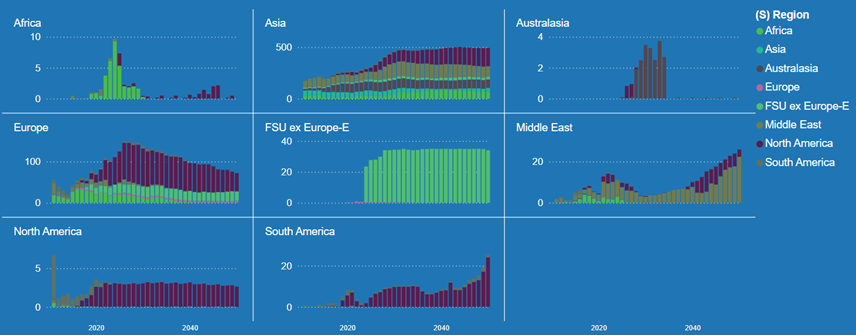

Saudi Arabia is also not the only country heavily investing in natural gas. RBAC recently published a commentary on how LNG heavyweight, Qatar, is further developing its impressive gas reserves, [13] while the United Arab Emirates is expanding its already robust LNG export capacity.[14] Qatar, Saudi Arabia, and the UAE have long been regional rivals due to their proximity to each other and making up a significant portion of the world’s natural gas and oil. Saudi Arabia and the UAE are in the top 5 oil producers globally. Qatar and the UAE are in the top 10 natural gas producers with Saudi Arabia also looking to enter this space.

All 3 of these countries are members of the Arab League which is a regional organization similar in nature to intergovernmental bodies such as NATO or the EU. However, despite this the members of the Arab League are often not as cooperative with each other as members of other organizations are. The most recent notable event was in 2017 when members of the Arab League cut diplomatic ties with Qatar and these ties were not restored until 2021. The investments into natural gas may potentially further strain the relationship between these countries.

To compete with its neighbors who are soon to become rivals in the natural gas space, Saudi Arabia is pumping large amounts of money to rapidly expand its gas infrastructure in order to take advantage of booming global demand for natural gas and LNG and bring competition for export contracts.

With the once high European demand projected to dwindle in response to energy transition policies, the gas that once flowed to this region is finding its way to customers in Asia. Saudi Arabia is looking to get in on the action and cement itself as not only a top producer of gas but for exports as well.

Where Does Renewable Energy Fit In?

In addition to investments into traditional energy sources, Saudi Arabia’s 2030 vision also includes adding significant amounts of renewable energy for power generation. Solar and wind are the primary sources of renewable energy within the country. “Saudi Arabia will tender new renewable energy projects with a capacity of 20 GW annually, aiming to reach between 100 and 130 GW by 2030, depending on electricity demand growth.”[15]

Conclusion

So, will Saudi Arabia and Aramco accomplish its gas and LNG goals?

It certainly seems the parts are in place to give it a fair shot. But to really accomplish these lofty goals, Saudi Arabia would greatly benefit from knowing how the market may change because of supply and demand fluctuations. A market as volatile and ever-changing as natural gas and LNG needs any potential disruptions to be accounted for. That is where the G2M2® Market Simulator for Global Gas and LNG™ can be of assistance. G2M2 can assist both countries and companies to find the best ways to achieve energy security, both in supply and production, through robust market analysis and better strategic decisions.

RBAC, Inc. has been the leading provider of market fundamental analysis tools used by the energy industry and related government agencies for over two decades. The GPCM® Market Simulator for North American Gas and LNG™ is the most widely used natural gas market modeling system in North America. RBAC’s G2M2® Market Simulator for Global Gas and LNG™ has been instrumental in understanding evolving global gas and LNG dynamics and is vital in fully understanding the interrelationship between the North American and global gas markets.

[2]https://jpt.spe.org/aramco-awards-7-7-billion-in-contracts-to-expand-fadhili-gas-processing-plant

[3]https://www.eenews.net/articles/saudi-aramco-signs-us-lng-deal/

[7]https://eigpartners.com/eigs-midocean-energy-completes-acquisition-of-20-percent-stake-in-peru-lng/

[9]https://oilprice.com/Energy/Natural-Gas/Aramco-Targets-60-Increase-in-Gas-Production-by-2030.html

[10] Ibid

[11]https://asia.nikkei.com/Business/Energy/Saudi-Arabia-eyes-100bn-bet-on-shale-gas-revolution-at-home.

[13] https://rbac.com/qatars-plans-for-vast-lng-expansion/

[14]https://www.naturalgasworld.com/uaes-well-timed-lng-expansion-global-gas-perspectives-112390