Similarly, The Double Prime Mover: Electricity Runs the Future, But Natural Gas Keeps It Running illustrates how accelerating electricity demand has tightened the coupling between power and natural gas markets (Figure 7), making system reliability increasingly dependent on their interaction.

In an energy-security-first environment, one cannot simply weigh stated policies, market signals, or investment flows in isolation, but the key is understanding the economic, market, and infrastructure constraints and where they are choking or glutting first, and how these translate through to prices, flows, and investment decisions across gas, power, and LNG markets.

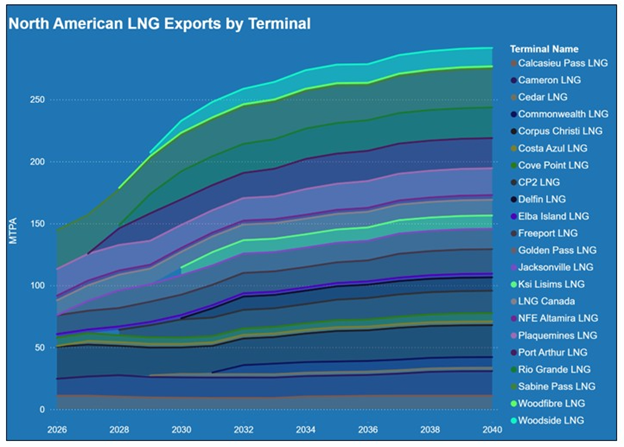

Conclusion: Energy Realism Takes Center Stage

Davos 2026 reflects a critical shift in how global leaders see energy. The conversation itself is increasingly anchored in energy security, encompassing reliability, affordability, infrastructure, and economic growth.

This change appears not to be rhetorical for it is grounded in experience: Germany’s reassessment of firm capacity, Europe’s response to supply shocks, grid failures that exposed system gaps, and demand growth that pushes the limits of deliverability.

Davos showed things can change. For natural gas, LNG, and power markets, this new take on energy matters. But talk may be cheap. Until policies (and contracts) are inked, the path forward may still be murky.

Markets are responding less to declarations and more to familiar market fundamentals, though the interactions between policy and markets are many, varied and complex. Understanding these market dynamics using advanced market simulation tools is what wins in an energy-security-first world.

Would you like a demonstration of RBAC’s market simulation tools? Click here for a demo or to contact us for more information.