Power to Change the World?

Power of Siberia 2 sounds like a Russia-China pipeline story. And on the surface (or below ground actually), that is exactly what it is. Russia needs new outlets for gas once aimed at Europe. China wants more energy security, more supply diversity, and fewer risks tied to long maritime routes and chokepoints such as the Strait of Hormuz.

Recent headlines show the project remains topical, yet price, timing, and the concern of swapping one dependency for another, continue to complicate a final deal.

So, the more important market question may be: what happens beyond Russia and China?

If Power of Siberia 2 enters service earlier than expected, the largest impact may not be the pipeline volume itself, but how that volume changes China’s next marginal gas purchase — plus, how many LNG cargoes will be produced or available to China and where will those LNG cargoes eventually go that China no longer needs?

That uncertainty is important. Power of Siberia 2 is not a done deal, so we shouldn’t write about it (as some have) as if it (or anything else) is a panacea to Asia’s energy hunger and growth, as well as its energy security.

But we can give new insights into both the project and its relationship to the greater global scene.

The Tension in the Room

One could argue that the project has moved forward politically, but commercially the path is thorny and complicated. Russia and China have definite reasons to want the pipeline, but they do not want it on the same terms.

That is the tension at the center of the story.

Russia has a clear need – produce and sell its gas. But the European market outlet has mostly evaporated; or at best, it is not as good as it once was for Russian pipeline gas, and that loss has changed the logic of Russian export strategy. A second large pipeline to China would give Moscow a long-term destination for gas that was once tied to Europe. From Russia’s point of view, Power of Siberia 2 is one of the most important pieces of its strategic pivot eastward.

China’s position is vastly different. Although it does have domestic energy, it is not nearly the energy powerhouse that Russia (or America) is. China is ten times larger than Russia in nearly every metric (population, GDP, trade volume), but actually they are quite similar (GDP, growth) per capita. Additionally, Russia has almost twice the land mass (and that’s part of the problem with Power of Siberia 2).

But outside of the U.S., Russia tops the list for oil and gas production. China wants supply security, but it also wants flexibility. But clearly it has not placed all its eggs in one basket. China wants a combination of increased pipeline gas, LNG, and domestic production, not to mention diversifying through continued coal, hydro and renewables, and nuclear. And perhaps above all, China wants to be in the driver’s seat — and likely would be with this project.

Yet, it hardly bears comment that China does not want to solve one vulnerability by creating for itself another. The project may be strategically attractive, but it is still commercially difficult. Beijing likely desires more Russian pipeline gas, especially with maritime routes looking less secure recently, yet not enough to trade import dependencies. Moreover, pricing is not in Moscow’s favor due to the fact that Beijing has other options.

So, when some recent headlines clamor that Power of Siberia 2 is going to solve all Russia’s and China’s problems, they may not be asking and answering the bigger question.

The Real Question

If we assume Power of Siberia 2 moves forward, however politically attractive or not, and if political and physical constraints in the Middle East intensify, what might be the global impact if the startup is earlier than expected? That is where scenario analysis becomes extremely useful, especially with tools like G2M2 Market Simulator for Global Gas and LNG.

So, the exact question RBAC analysts looked at is: “If Power of Siberia 2 is built sooner, how does the global gas market respond?” Does China simply consume more gas? Does it import less LNG? Do displaced cargoes move to Europe? Do Asian and European benchmark prices change? And if so, by how much?

These are the kinds of questions that cannot be answered by looking at the pipeline in isolation. Power of Siberia 2 may be physically buried across Russia, Mongolia, and China, but its market consequences would reverberate throughout LNG trade routes, regas terminals, storage balances, and price signals around the world.

A Short Review

Power of Siberia 2 is not a new topic for RBAC.

Having begun its modeling and analytical efforts in 1997 when deregulation was really hitting its stride in the United States, RBAC has not only watched, but contributed to the formation of a mature US gas market (see What the Data Shows Us About Building Natural Gas Pipelines Part 3) with the development and support of the GPCM Market Simulator for North American Gas and LNG.

The transformation from disconnected regional markets integrating into a truly global market has been made possible through LNG trade, as we wrote about in Japan’s LNG Energy Security Has a Cost. There we also noted how Europe and Asia competed for the same cargoes and where local fundamentals in one region affect prices in another. In that report, Power of Siberia 2 was mentioned as one of the infrastructure options that could change China’s demand for LNG over time.

But China’s demand waxes and wanes, as it juggles its own import policies in attempts to match demand growth with energy supply and prices. In LNG Exporters Grip with Uncertainty Over Chinese LNG Demand, we looked at how China was already balancing between domestic production, pipeline gas, LNG imports, and even LNG resales. Even then, the question had changed from simply whether China would consume more gas to how would Chinese buyers play their cards in the global market, a market wherein more Russian pipeline gas was available.

Then in China’s LNG Surge: Surpasses Japan as Top LNG Importer, we saw the other side of the story. China’s domestic demand recovered in 2023, and LNG imports rebounded strongly, once again making China the world’s largest LNG importer. Yet even with renewed enthusiasm, LNG was only one part of China’s energy future. China has domestic gas production and pipeline imports, and if Power of Siberia 2 comes online in the 2030s, total pipeline gas imports could increase significantly.

But that future has been evolving. In From Russia to the Rest, we looked at what happens as Europe reduces or eliminates (per its own policies) Russian gas from its supply mix. Russia still has gas to sell. Europe still needs replacement supply. Asia becomes more important. LNG and even pipeline flows shift. Energy options become more strategic. Power of Siberia 2 thus begs the question: if Russian gas does not go west, where does it go, and what happens to the rest of the market?

And in RBAC’s 25Q4 Global Gas Market Overview, we looked at a global gas market entering a new phase: Europe balancing storage tightness with the phase-out of Russian gas, Asia continuing to drive global demand growth, and North America scaling up LNG exports into the mid-2030s, with all these trends interacting.

And now with the war in Iran competing for global attention with the war in Ukraine, the world is looking with renewed urgency for supply security and diversity, as we reported in Middle East Disruption, European Storage, and the Next LNG Supply Wave.

Bringing It All Together

Power of Siberia 2 is a useful case study because it brings together nearly every major theme in the global gas market today: Europe’s pivot away from Russia while scrambling for replacement, Russia’s need for a major new market, China’s search for supply security and diversity, North America’s export growth, Asia’s demand trajectory, and the question of how flexible the global LNG market really is.

Shell’s recent release of its 2026 LNG Outlook adds another useful market reference point, elucidating how China acts as a key balancing force in the global gas market, with domestic production, pipeline imports, and LNG imports all giving it flexibility; also noting that China’s gas market continues to grow even as LNG imports moderate, precisely due to domestic production and pipeline imports.

With all that said, although the IF question gets the most attention, one might say the WHEN question will be very insightful. That is very close to the question we are asking here.

How could an earlier startup of Power of Siberia 2 change China’s gas supply stack, reduce China’s need for marginal LNG, and push those cargoes into other parts of the world?

Early Start Scenario

In the base (reference) case, Power of Siberia 2 begins moving gas in 2035. In the Early Start scenario, the online date is moved forward to 2032.

It is a simple but revealing G2M2 scenario: what happens if a 50 bcm/year pipeline arrives three years earlier than expected?

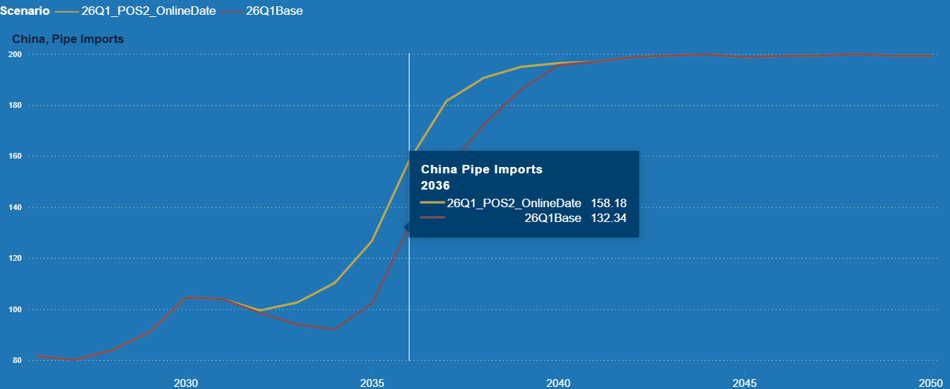

Pipeline imports into China (Figure 2) increase to ~158 bcm by 2036, ~25 bcm more than the base case. That is the direct effect of the earlier online date.

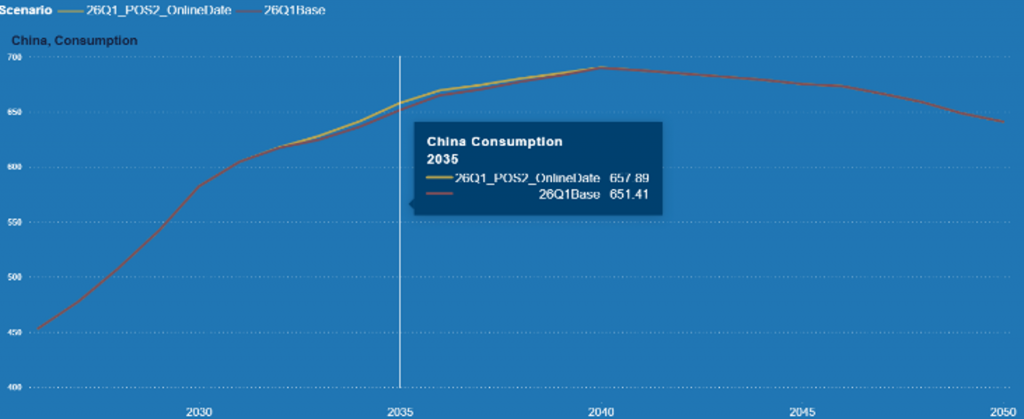

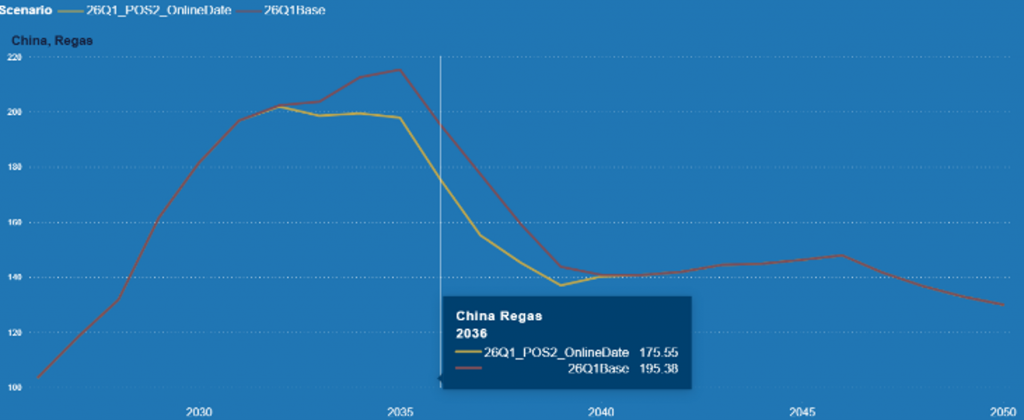

And China’s gas balance adjusts: By 2036 in the scenario, Chinese annual gas consumption (Figure 3) increases by about 5 bcm, while LNG regasification (Figure 4) falls by almost 20 bcm with these trends moderating after 2036.

That is the market mechanism. Power of Siberia 2 changes China’s marginal gas purchases. Some of the new pipeline gas supports additional consumption, but a meaningful portion replaces LNG that China otherwise would have needed.

This is why the global effect matters. LNG cargoes do not disappear. They move to other markets.

In the G2M2 results, we see that lower Chinese demand for LNG changes global LNG flows. LNG deliveries into China fall by 2.30 bcm/year from Australia through 2040, 0.197 bcm/year from North America, and 5.55bcm/year from other supply regions during the early years of the scenario. Some of those cargoes are absorbed elsewhere in Asia, while Europe sees regasification increase by 5.72 bcm/year in 2033 and another 4.51 bcm/year in 2034.

That is how connected Global LNG now is.

Europe is phasing out Russian gas, yet still needs supply for storage, power, industry, and winter reliability. China taking more Russian pipeline gas does not also send gas to Europe. But China’s portfolio players can send LNG cargoes westward for Europe, or other importing regions, to absorb.

So, there is an interesting market irony here: Russian pipeline gas going east can help make more non-Russian LNG available west.

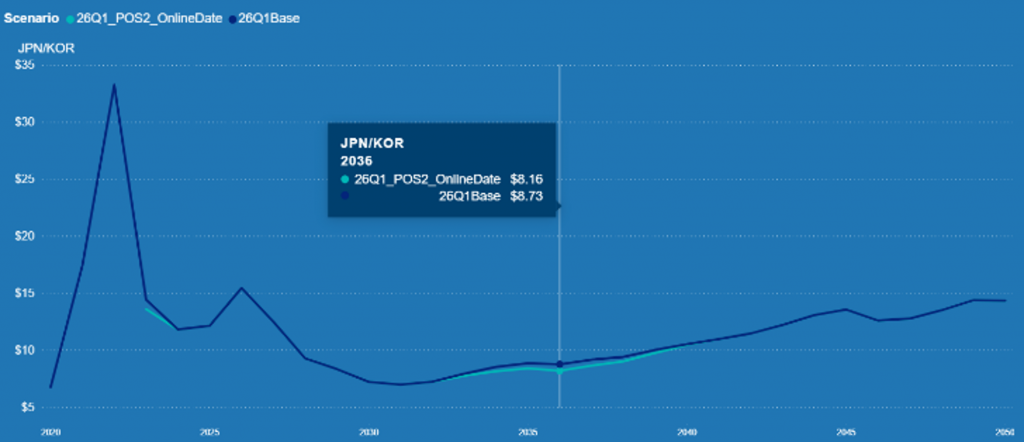

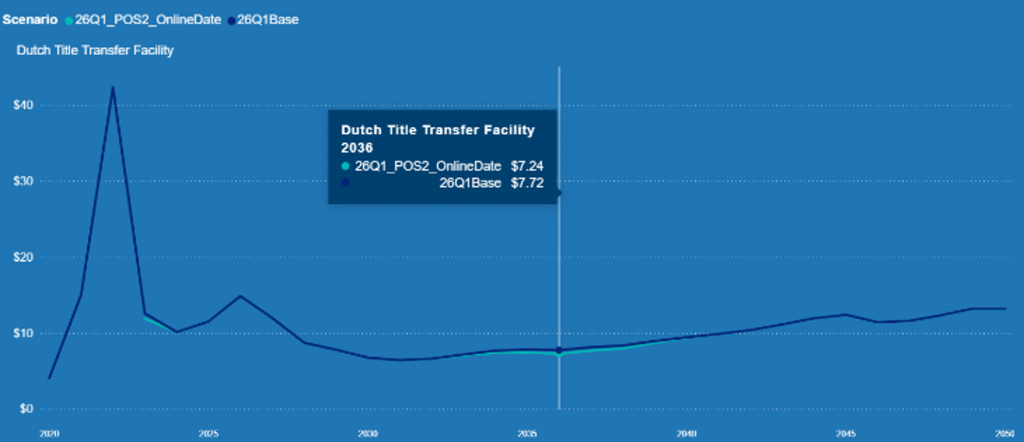

Prices move in the same direction. By 2036 in the scenario, Japan Korea price (Figure 5) falls to approximately $8.16/MMBtu or –6.5% in 2036, while TTF (Figure 6) falls to around $7.24/MMBtu or –6.29% before starting to recover. The change is not catastrophic or market breaking. It is modest. But it is directionally important because it shows how pipeline timing in one region can influence benchmark prices in another.

approximately $8.16/MMBtu or –6.5% in 2036, while TTF falls to around $7.24/MMBtu or –6.29% before starting to recover. The change is not catastrophic or market breaking. It is modest. But it is directionally important because it shows how pipeline timing in one region can influence benchmark prices in another.

A Summing Up

So, Power of Siberia 2 is really about changing where China gets its next unit of gas.

When China’s supply stack shifts, LNG trade shifts. When LNG trade shifts, Europe and Asia feel it. When Europe and Asia feel it, prices respond.

So, it is not only important whether Power of Siberia 2 gets built, but when. Even with the same pipe, same route, same capacity, you can end up with a different market.

Just 5 years ago, Nord Stream 2 was on the precipice of completion. Just 5 months ago the world was facing a supply glut, and a fierce competition around LNG exports between Qatar and the U.S. in particular. Yet, geopolitics can knock the game pieces over and when they are upright again, they will not be in the same place as they were.

By 2032, how the global LNG market will look, is an interesting question. It could be digesting a new LNG supply wave, Europe could still be rebuilding its post-Russian gas system, and Asia could be pulling more gas into power, industry, transport, and data center demand. If a large pipeline starts up as well, the seemingly bilateral story, will effect global changes: in Chinese regas terminals, European storage tanks, LNG shipping routes, and benchmark price curves.

Power of Siberia 2 could matter far beyond Russia and China.

RBAC’s market simulation tools can give insight into the natural gas market under a wide range of scenarios, including cases where geopolitics, infrastructure, demand growth, weather, or project timing move differently than expected. To discuss a scenario or schedule a free demonstration, contact RBAC.

RBAC, Inc. has been the leading provider of market fundamental analysis tools used by the energy industry and related government agencies for over two decades. The GPCM® Market Simulator for North American Gas and LNG™ is the most widely used natural gas market modeling system in North America. RBAC’s G2M2® Market Simulator for Global Gas and LNG™ helps users understand evolving global gas and LNG dynamics and the interrelationship between North American and global gas markets.