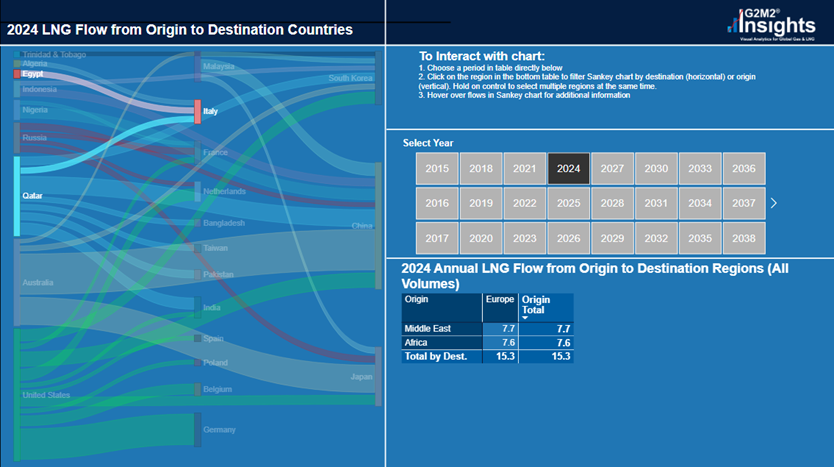

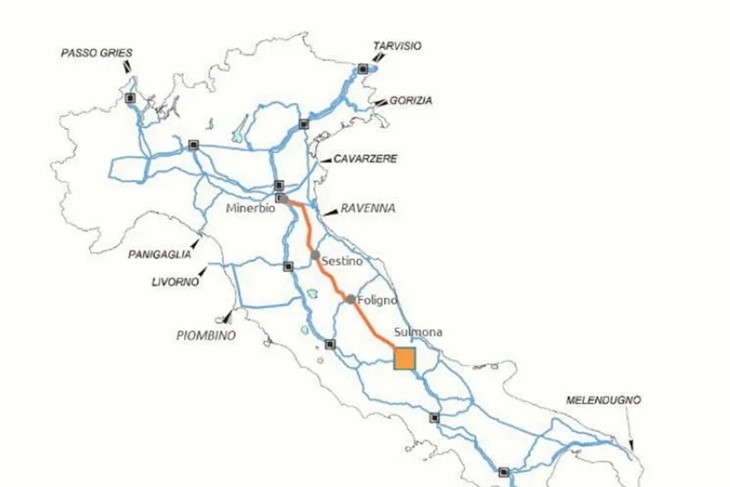

Currently, the only way Italy will be able to send gas to the rest of Europe is through existing pipelines or those under construction as it does not currently have any LNG export terminals, nor any plan to build such in the future. However, if Italy sees success from its efforts towards becoming a gas hub, then it wouldn’t be out of the realm of possibility for LNG export proposals to follow as most current pipelines within the country possess the ability to reverse flows.

But where would the supply of gas flowing into Italy and through these pipelines come from? The African nations of Algeria, Egypt, and Libya would likely be the primary suppliers of natural gas that would go on to reach Europe, while the Republic of Congo and Angola may also become part of this supply chain. Algeria and Libya possess Africa’s second and fourth largest proven gas reserves. Algeria has long been a key supplier to Europe, especially to France and Italy, but this new plan would further expand its role while introducing new natural gas suppliers into Europe. However, with the European Union pushing for an accelerated energy transition, the demand for gas may carry increased uncertainty and volatility through the coming decades. But what we can be sure of is that gas will still have a significant presence within the European energy mix for many years to come.

Irregardless, Italy seems set on becoming the natural gas gateway from Africa to the European market, and to this end, it is investing massive resources and capital to make this dream a reality. Of course, Africa also has its own plans for utilizing the abundant domestic resources to provide affordable and reliable sources of energy and in the words of the late President of Namibia, Hage Geingob, “Benefits from African resources must benefit Africa.”

Italy appears to be taking this to heart; and a project of this scale would be impossible if not for the full support of all parties involved. At the recent Italy-Africa summit in Rome, leaders from several African countries and organizations convened with representatives from the European Union wherein a commitment to the development of Africa was solidified and assurances made that the benefits of these gas exports will be seen by Africans as well. The Chairperson of the African Union Commission, Moussa Faki, stated that the goals outlined in the Mattei plan align with Africa’s priorities. While the President of the European Parliament, Roberta Metsola proclaimed, “When Africa prospers, Europe prospers and the whole world can.”

For this grand undertaking, it is imperative that market analysts and policy makers have the tools and knowledge necessary to explore all options towards meeting these enormous goals. RBAC’s G2M2® Market Simulator for Global Gas and LNG™ can be used to assess the viability and effects that any project or changes in policy would have on supply, demand, prices, and gas flows. It is with tools like G2M2 that both industry and government can find the best ways to achieve energy security for themselves and others, both in supply and production, through robust market analysis and better strategic decisions.

RBAC, Inc. has been the leading provider of market fundamental analysis tools used by the energy industry and related government agencies for over two decades. The GPCM® Market Simulator for North American Gas and LNG™ is the most widely used natural gas market modeling system in North America. RBAC’s G2M2® Market Simulator for Global Gas and LNG™ has been instrumental in understanding evolving global gas and LNG dynamics and is vital in fully understanding the interrelationship between the North American and global gas markets.